Introduction

Many global companies plan to invest in ASEAN as they expand production, diversify supply chains, and access new consumer markets. The region offers strong economic growth, improving infrastructure, and competitive manufacturing ecosystems. As a result, ASEAN continues to attract foreign direct investment across sectors such as manufacturing, digital infrastructure, energy, and services.

However, ASEAN is not a single market. Regulatory frameworks, labor structures, and infrastructure readiness vary widely across countries. These differences influence where investors allocate capital and how they structure market entry.

In this guide, we at Source of Asia outline the ASEAN investment landscape in 2026. It highlights major investment trends, key sectors attracting capital, and practical considerations companies should evaluate before entering the region.

Key Insights

- Foreign investment concentrates in major markets such as Singapore, Indonesia, Vietnam, Malaysia, and Thailand, where infrastructure, industrial ecosystems, and market scale support large projects.

- Global supply chain diversification is accelerating investment, as multinational companies expand production networks across Southeast Asia to reduce reliance on single-country manufacturing bases.

- Manufacturing, digital infrastructure, and energy projects remain the primary sectors attracting foreign capital due to rising regional demand and ongoing industrial development.

- Government incentives support foreign investment, particularly through tax benefits, special economic zones, and industry-focused programs designed to attract strategic sectors.

- Country-level differences influence investment decisions, including variations in labor costs, infrastructure readiness, regulatory procedures, and administrative efficiency across ASEAN markets.

Investment Landscape for Companies Looking to Invest In ASEAN

ASEAN continues to attract strong investor interest as regional economies expand and supply chains evolve. Understanding current investment trends, FDI flows, and production shifts helps explain how capital is being allocated across the region.

ASEAN’s investment landscape in 2026

The Association of Southeast Asian Nations (ASEAN) has become one of the most relevant investment regions in Asia. The bloc brings together economies with a combined population of more than 680 million people and a rapidly expanding middle class. This creates both large manufacturing capacity and strong domestic demand.

Economic growth across the region has remained relatively stable, with several ASEAN economies expected to grow at 4%-5% annually through 2026. For international investors planning to invest in ASEAN, this combination of market scale, steady growth, and improving regional integration continues to position ASEAN as a practical base for long-term business expansion in Asia.

Recent FDI inflows across the region

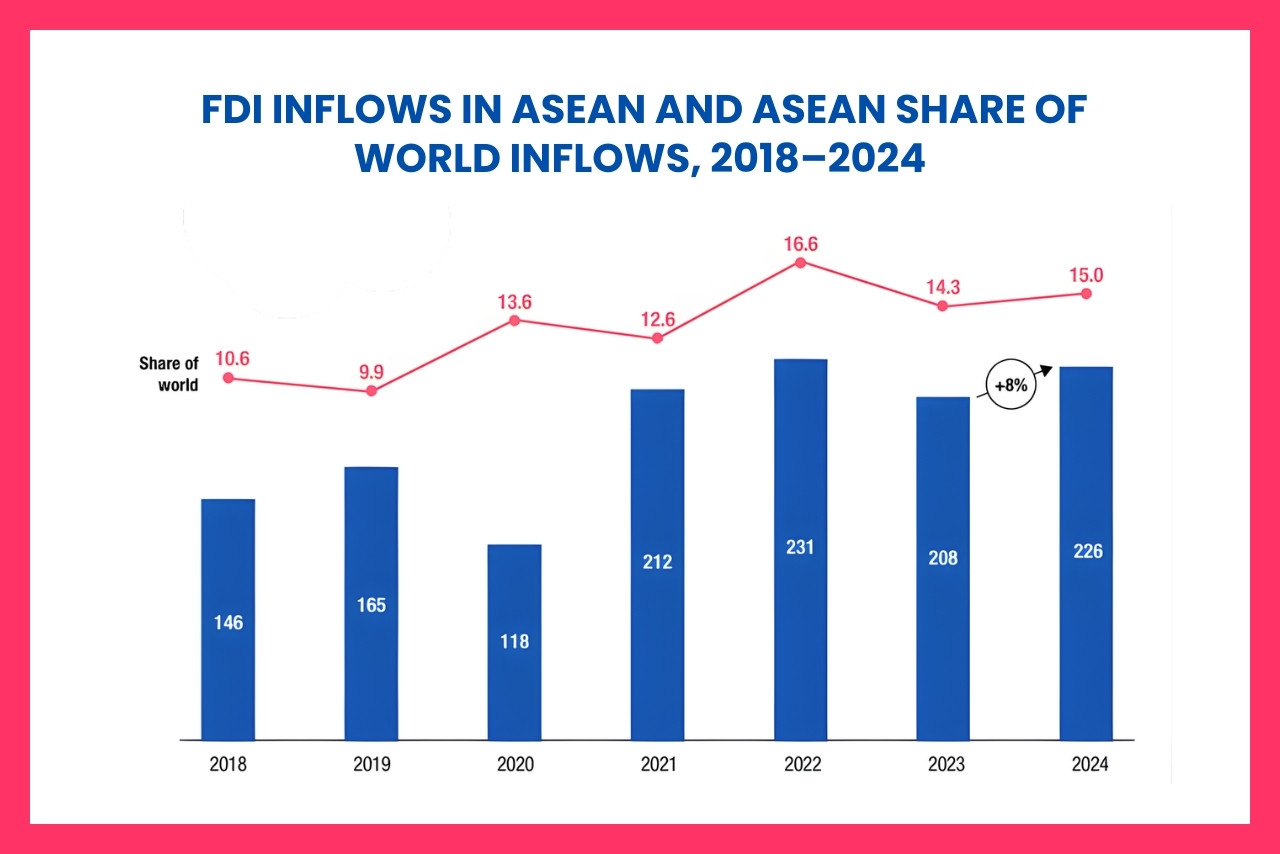

ASEAN’s investment landscape in 2026 remains resilient despite global uncertainty. Data from the ASEAN Investment Report 2025 show that the region attracted approximately $226 billion in FDI in 2024, an 8% increase, while global FDI declined by 11%. ASEAN has received more than $200 billion in annual FDI since 2021, significantly higher than the pre-pandemic average of about $130 billion.

Investment remains concentrated in several key markets, particularly Singapore, Indonesia, Vietnam, and Malaysia. These countries continue to attract capital into manufacturing, electronics, financial services, and digital infrastructure.

FDI inflows in ASEAN and ASEAN’s share of world inflows in 2018-2024 (ASEAN investment report 2025)

How global supply chain shifts influence investment

Changes in global supply chains are also shaping where companies choose to invest in ASEAN. Many multinational firms are adopting China+1 strategies, reducing reliance on single-country production models while expanding operations across multiple Asian markets. As part of this shift, ASEAN countries are increasingly integrated into manufacturing networks for electronics, automotive components, and semiconductors.

Governments across the region are encouraging this transition through new industrial parks, improved logistics infrastructure, and investment incentives designed to attract relocated production. As a result, supply chain diversification is likely to remain a key driver of new investment projects in ASEAN over the coming years.

Key Sectors Driving Companies To Invest In ASEAN

Investment opportunities in ASEAN are increasingly concentrated in key sectors such as manufacturing, digital infrastructure, and sustainable energy, where regional demand and policy support continue to drive growth.

Manufacturing and industrial development

Manufacturing remains one of the strongest investment drivers for companies looking to invest in ASEAN. Countries such as Vietnam and Indonesia are becoming major production hubs as global companies diversify supply chains and expand regional operations.

Several structural factors support this trend:

- Competitive labor markets compared with traditional manufacturing centers

- Expanding industrial parks and export-oriented production zones

- Stronger integration into regional trade frameworks such as the Regional Comprehensive Economic Partnership (RCEP)

Electronics assembly, automotive components, and consumer manufacturing are among the sectors receiving sustained foreign investment as production networks continue to expand across ASEAN.

Digital infrastructure and technology

Digital infrastructure is another rapidly growing investment area. Southeast Asia’s digital economy is projected to exceed $330 billion by 2025, according to the International Trade Administration, driven by growth in e-commerce, fintech, and digital services.

Investment activity is concentrated in several areas:

- 5G network expansion and telecommunications infrastructure

- Cloud computing and data center development

- Cybersecurity and digital platform ecosystems

Regional initiatives are also accelerating digital transformation. Singapore’s Smart Nation Initiative and Thailand’s Thailand 4.0 strategy illustrate how governments are actively supporting technology development and digital innovation.

Energy and sustainable infrastructure

Energy demand across ASEAN continues to increase alongside industrial growth and urban expansion. At the same time, governments are introducing policies to support energy transition and reduce carbon intensity.

Current investment priorities include:

- Utility-scale solar and wind energy projects

- Grid upgrades and energy transmission infrastructure

- Sustainable urban infrastructure and green transport systems

These sectors continue to attract both public and private capital as countries seek to balance economic growth with long-term energy security.

For a more detailed breakdown of sector-specific opportunities across ASEAN markets, you can explore Sectorial Notes – Source of Asia to have a deeper analysis of industry trends and investment developments in the region.

Key sectors attracting investment include manufacturing, electronics, digital services, and infrastructure development.

Policy Environment And Investment Incentives For Companies Invest In ASEAN

Government policies across ASEAN are designed to attract foreign capital while supporting national development priorities. For companies planning to invest in ASEAN, investors typically evaluate three policy dimensions when entering the region: government promotion programs, fiscal incentives, and ownership regulations.

Investment promotion and government incentives

National Investment Promotion Agencies (IPAs) play a central role in attracting foreign projects and guiding investors through regulatory procedures. These institutions provide market information, licensing support, and access to government incentive programs for priority sectors such as manufacturing, technology, and renewable energy.

In many ASEAN markets, incentive frameworks typically focus on three areas:

- Priority industry programs that encourage investment in strategic sectors.

- Infrastructure development linked to industrial parks and logistics corridors.

- Administrative reforms that streamline investment approvals and reduce entry barriers.

Tax incentives and special economic zones

Tax incentives remain one of the most widely used policy tools to attract foreign direct investment. Depending on the country and industry, investors may benefit from corporate income tax reductions, tax holidays, or exemptions on import duties for machinery and production inputs.

Special economic zones (SEZs) and industrial parks further support investment by offering simplified customs procedures, dedicated infrastructure, and preferential regulatory conditions. These zones are widely used across ASEAN to accelerate industrial development and facilitate export-oriented production.

Foreign ownership and regulatory conditions

Foreign ownership regulations vary across ASEAN countries, but most markets have gradually liberalized their policies to encourage international participation. In many sectors, foreign investors can establish wholly owned subsidiaries, while some strategic industries may still require local partnerships or joint venture structures.

Regulatory conditions also differ in areas such as licensing procedures, land-use rights, and sector-specific restrictions across ASEAN markets. Because of these differences, investors typically assess country-level regulations carefully before selecting the most suitable market entry structure.

Where Investors Choose To Invest In ASEAN

Investing in ASEAN is concentrated in a few key economies where infrastructure, market size, and policy frameworks support large-scale projects. At the same time, country-level differences continue to influence how investors select their entry markets.

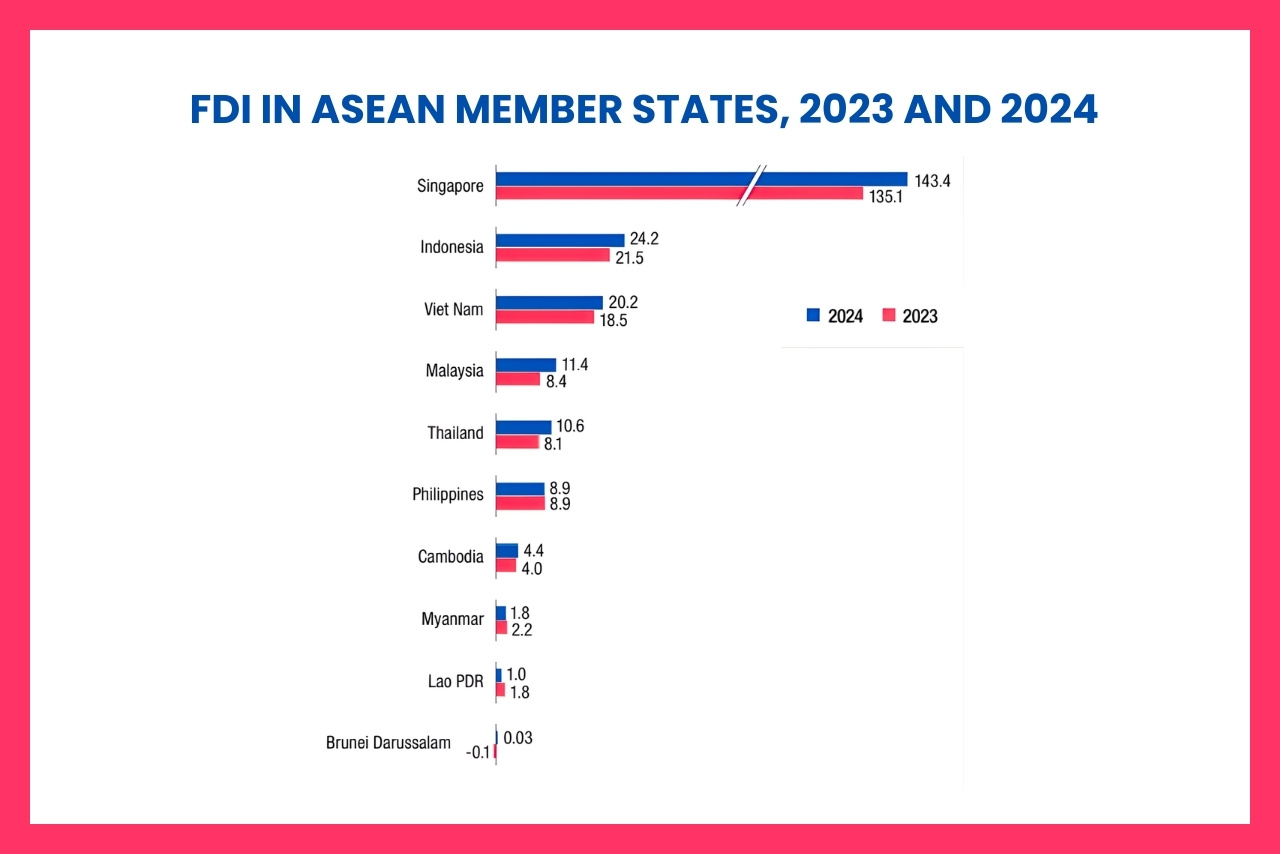

FDI inflows across ASEAN member states in 2023 and 2024 (ASEAN investment report 2025)

Leading recipient countries

Foreign investment across ASEAN remains concentrated in several key economies. Singapore continues to lead the region, attracting around USD 143 billion in FDI in 2024, largely due to its role as a regional financial hub and headquarters location for multinational companies.

Meanwhile, Indonesia and Vietnam have emerged as major destinations for manufacturing and industrial investment, receiving roughly USD 24 billion and USD 20 billion. Malaysia and Thailand also continue to attract steady capital, particularly in digital infrastructure, advanced manufacturing, and energy-related projects.

Country-level differences that influence entry decisions

Although ASEAN operates as a regional bloc, investment conditions differ significantly across countries. These differences often shape how and where companies allocate capital when they invest in ASEAN.

Several factors typically influence market entry decisions:

- Labor structure: Workforce size, wage levels, and availability of skilled labor vary across markets.

- Infrastructure readiness: Transport networks, logistics capacity, and industrial zones affect operational efficiency.

- Administrative efficiency: Regulatory procedures, licensing timelines, and investment approvals differ between jurisdictions.

Because of these variations, investors often compare multiple ASEAN markets before selecting a primary investment location.

For a detailed comparison of individual markets and investment conditions, you can explore Country Profiles – Source of Asia.

Common Challenges When Companies Invest In ASEAN

Although ASEAN continues to attract strong investment inflows, companies planning to invest in ASEAN should also be aware of several practical challenges. These issues often relate to regulatory structures, operational conditions, and local business practices, which vary across ASEAN markets.

- Regulatory and administrative complexity: Investment procedures and regulatory frameworks differ across ASEAN countries. In some markets, investors must coordinate with multiple government agencies, and sector-specific rules may extend licensing and approval timelines.

- Operational and infrastructure constraints: Conditions for logistics, transport networks, and energy reliability vary across the region. These differences can influence supply chain efficiency, particularly for manufacturing and infrastructure-intensive operations.

- Governance and cultural considerations: Differences in local management practices, communication styles, and decision-making processes may affect coordination with partners and local stakeholders during project implementation.

Practical Considerations Before You Invest in ASEAN

Before committing capital in ASEAN markets, investors typically evaluate several operational and structural factors. Market entry models, tax structures, and expansion strategies can significantly influence both compliance requirements and long-term business performance.

- Structuring market entry and entity setup: Companies entering ASEAN often choose from a representative office, a joint venture, or a wholly owned subsidiary, depending on regulatory conditions and operational goals. Each structure involves different levels of control, investment commitment, and compliance obligations.

- Tax planning and cross-border compliance: Investment projects should account for corporate tax structures, transfer pricing exposure, and cross-border reporting requirements. These considerations are particularly important for multinational companies operating across several ASEAN jurisdictions.

- Phased expansion strategy: Many investors adopt a phased market entry approach, starting with limited operations to assess market conditions before making larger capital commitments. This allows companies to test demand, build local partnerships, and adapt their strategy before scaling operations.

Final Thoughts

ASEAN continues to attract international investors seeking to invest in ASEAN, thanks to its diverse economies, expanding supply chains, and growing consumer markets. While each country presents different regulatory conditions and operational realities, the region offers meaningful opportunities for companies seeking long-term growth in Asia.

At Source of Asia, we support companies throughout the investment journey in ASEAN. Our experts help evaluate market potential, conduct market diagnosis and competitor analysis, identify qualified local partners, and support on-the-ground development across Southeast Asia.

To support further preparation, the following insights may provide additional context for evaluating ASEAN market opportunities:

Frequently Asked Questions

The best location depends on business goals. Singapore leads as a regional financial and headquarters hub, while Indonesia and Vietnam attract manufacturing investment due to market size and industrial growth. Malaysia and Thailand also receive steady capital in the technology and energy sectors.

Foreign investment in ASEAN is largely driven by manufacturing, digital infrastructure, and energy projects. Supply chain diversification supports industrial production, while rapid digital adoption increases demand for technology infrastructure, data centers, and telecommunications networks across the region.

Foreign companies typically enter ASEAN through a representative office, joint venture, or wholly owned subsidiary. The appropriate structure depends on sector regulations, investment size, and long-term plans, as licensing requirements and ownership rules differ across ASEAN markets.