Introduction

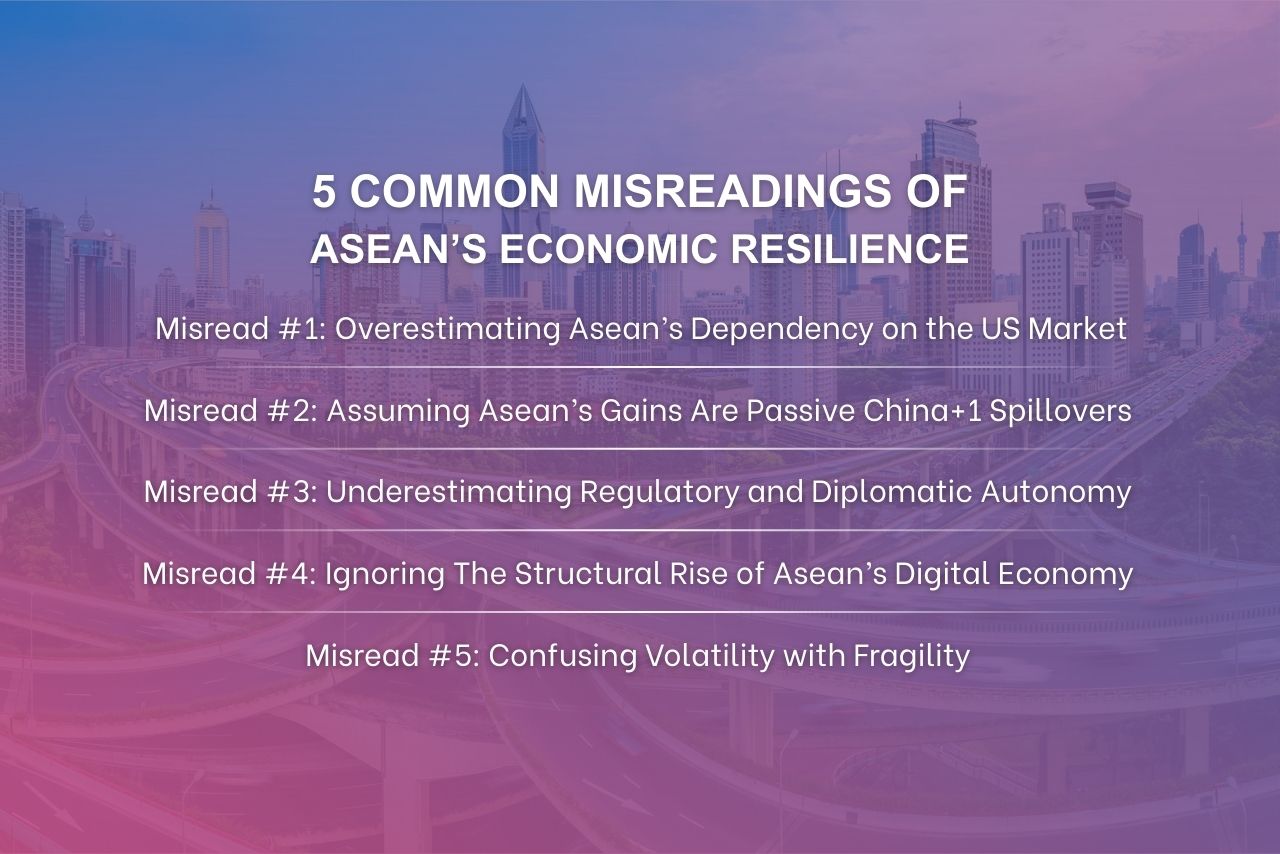

ASEAN’s economic resilience in 2026 is often misunderstood by US executives evaluating expansion or supply chain strategy in Southeast Asia. Many still view the region as a secondary beneficiary of China+1 shifts, or a fragile group of emerging markets, or an economy largely dependent on exports.

In practice, resilience is supported by diversified trade relationships, deeper regional integration, growing domestic demand, and increasingly adaptive policy frameworks.

In this article, we – Source of Asia, explain several common misreadings of ASEAN’s economic resilience and explain why they matter. Understanding these dynamics helps companies assess market entry, supply chain positioning, and long-term investment strategies in Southeast Asia.

Key Insights

- ASEAN’s growth is supported by diversified global trade partnerships, not reliance on a single major market

- The region is emerging as a structural manufacturing and supply chain hub, beyond the simple China+1 strategy

- ASEAN governments maintain strategic policy autonomy, balancing relations among major global powers

- The digital economy is becoming a major long-term growth driver across ASEAN markets

- Economic volatility often reflects adaptive policy capacity and structural resilience, not underlying fragility

What Is Economic Resilience in Emerging Markets?

Understanding economic resilience helps companies assess how emerging markets manage shocks, maintain growth, and adapt to change, particularly across diverse countries in Southeast Asia.

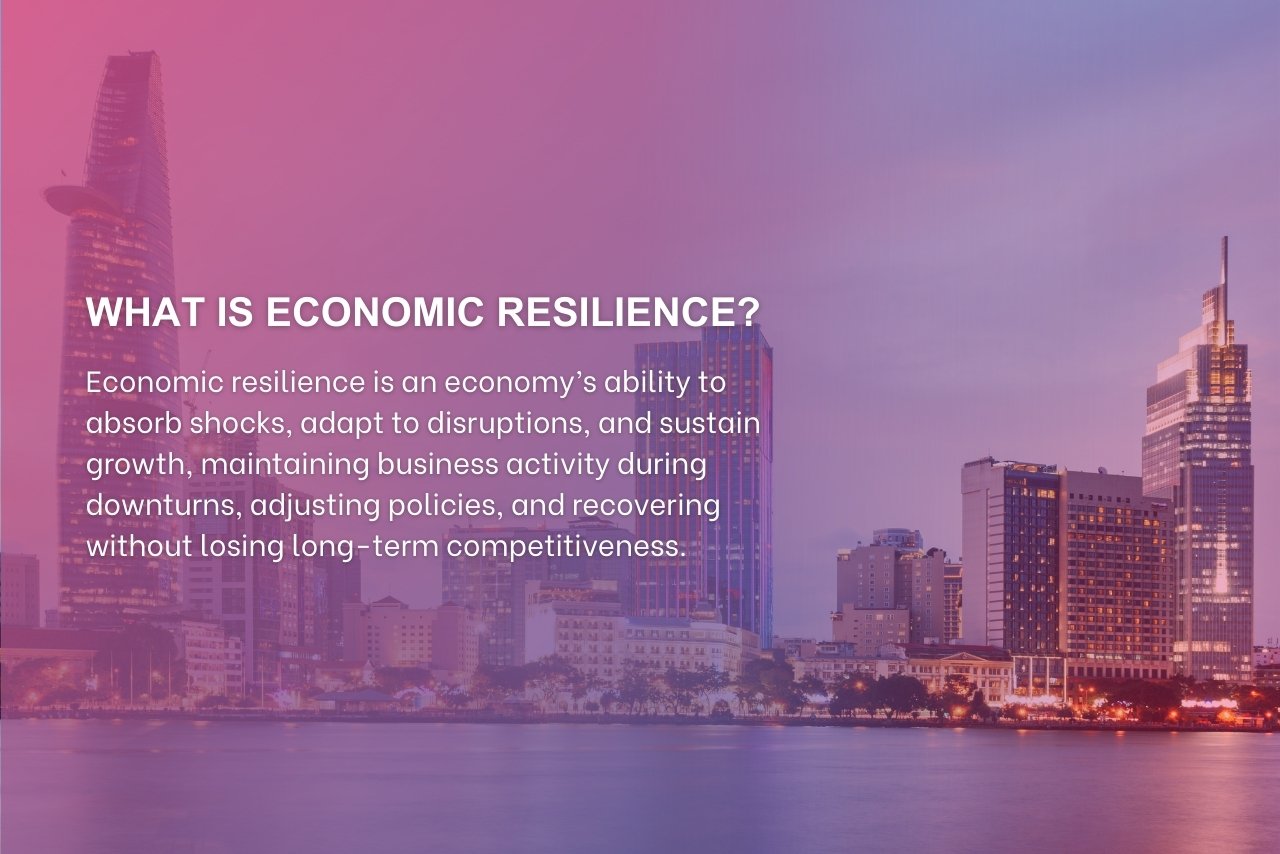

What is economic resilience?

Economic resilience refers to an economy’s ability to absorb shocks, adapt to disruptions, and continue growing over time. In practice, this means the economy can maintain business activity during downturns, adjust rules when conditions change, and recover without losing long-term strength.

According to McKinsey & Company, resilience is more than just the ability to recover quickly. Recovery focuses on returning to pre-crisis levels after disruption. Resilience focuses on stability during the shock and the capacity to adapt while conditions remain uncertain.

For companies evaluating emerging market resilience, this difference matters. Economies with stronger resilience typically provide more predictable operating conditions, even when global markets experience volatility.

Economic resilience refers to an economy’s ability to absorb shocks and sustain growth.

Key elements of this diversification include:

- Strong intra-ASEAN trade, supported by integrated manufacturing and logistics networks across member states. The report ASEAN Economic Community Strategic Plan 2026 – 2030 shows that intra-ASEAN trade has represented over one-fifth of ASEAN’s total trade.

- China as a major trading partner, both as a production input source and a large export destination

- Expanding trade relationships with the EU, Japan, South Korea, and other Asian markets.

Rise of intra-regional supply chains

Another structural factor is the increasing integration of regional supply chains across ASEAN economies. Manufacturing activities are no longer concentrated in a single country. Instead, production stages are distributed across several locations depending on cost structures, industrial specialization, and logistics advantages.

For example, electronics supply chains often link Malaysia, Vietnam, and Thailand, while automotive components move between Thailand, Indonesia, and Vietnam. These production networks allow companies to optimize sourcing and assembly across the region.

In addition, the Regional Comprehensive Economic Partnership (RCEP) effect strengthens this integration by lowering tariffs and simplifying rules of origin, making cross-border manufacturing easier to manage.

Domestic demand as a shock absorber

Beyond external trade, domestic consumption increasingly supports ASEAN’s economic resilience strategies. Internal demand across the region has grown rapidly and now plays a larger role in sustaining economic activity.

Several structural trends contribute to this shift:

- A rising middle class, driving household consumption

- Rapid urbanization, especially in large metropolitan areas

- Growth in digital consumption, including e-commerce and digital services

Thus, domestic markets now act as a buffer when global trade slows, helping ASEAN economies maintain more stable growth.

Misread #2: Assuming Asean’s Gains Are Passive China+1 Spillovers

Many investors believe ASEAN’s recent growth mainly comes from companies relocating production from China. However, China+1 acts as a catalyst, while ASEAN governments actively shape industrial development.

China+1 is a catalyst, not the core driver

China+1 has accelerated manufacturing shifts, but it does not fully explain ASEAN’s economic momentum. Over the past decade, governments across Southeast Asia have positioned their economies through deliberate policy choices, for example:

- Vietnam’s industrial policies prioritize electronics, semiconductors, and high-tech manufacturing.

- Malaysia’s national industrial plans focus on advanced manufacturing and semiconductor ecosystems.

- Singapore’s economic strategy emphasizes technology, innovation, and high-value services.

These initiatives demonstrate that ASEAN policy positioning is proactive, not reactive to global supply chain shifts.

Industrial policy and strategic positioning

ASEAN governments are increasingly developing industry-focused manufacturing ecosystems, supported by targeted policies and investment incentives that attract higher-value production activities.

Key sectors attracting investment include:

- Semiconductor manufacturing and packaging: Malaysia, Singapore, and Vietnam strengthening chip testing and assembly capabilities.

- Electric vehicle supply chains: Thailand and Indonesia promoting EV production, batteries, and supporting components.

- Electronics manufacturing clusters: Vietnam, Malaysia, and Thailand hosting major regional production networks.

According to the World Economic Forum, over 90% of manufacturers now prioritize regionalized supply chains, reinforcing Southeast Asia’s role in advanced manufacturing networks.

From low-cost manufacturing to value chain upgrade

ASEAN economies are gradually moving beyond low-cost manufacturing toward higher-value activities. Governments and companies are increasingly investing in three key areas:

- Technology adoption included automation and digital manufacturing

- Workforce upskilling supported by technical education and industry training programs

- Moving up the global value chain with ASEAN firms participating in design, engineering, and specialized production

Thus, ASEAN is evolving from a cost-driven production base into a more capable manufacturing and technology ecosystem.

| To understand how these structural shifts translate into sector-level opportunities and policy alignment, explore our ASEAN–U.S. Business Outlook 2026–2030 booklet. |

ASEAN’s growth is driven by internal reforms, not only China+1 supply chain shifts.

Misread #3: Underestimating Regulatory and Diplomatic Autonomy

One common mistake is that ASEAN’s policy space is limited by major power competition. In practice, the region works through multi-directional diplomacy, varied trade rules, and regional cooperation systems.

ASEAN’s multi-vector diplomacy

ASEAN governments rarely align exclusively with a single global power. Instead, most countries follow a non-aligned strategy, maintaining economic and diplomatic engagement with the United States, China, and the European Union while prioritizing domestic development objectives.

In practice, this creates a pragmatic hedging approach. ASEAN economies maintain technology and investment links with the U.S., sustain strong trade integration with China, and expand regulatory and market cooperation with the EU. This balance helps governments reduce geopolitical exposure when tensions emerge between major powers.

Trade agreements as resilience tools

Trade agreements are an important tool that helps strengthen ASEAN’s economic resilience strategies and policy flexibility. By participating in multiple regional and bilateral frameworks, ASEAN economies expand market access while reducing dependence on any single trading partner.

Some trade agreements shaping this environment:

- CPTPP (Comprehensive and Progressive Agreement for Trans-Pacific Partnership): Expands access to markets such as Japan, Canada, and Australia while strengthening rules on investment and digital trade.

- RCEP (Regional Comprehensive Economic Partnership): The world’s largest trade agreement linking ASEAN with China, Japan, South Korea, Australia, and New Zealand.

- Bilateral FTAs with partners in Asia and Europe: Help diversify export destinations and stabilize long-term trade relationships.

Institutional evolution

Over the past two decades, ASEAN economies have gradually strengthened regional institutions to manage financial and economic volatility more effectively. One major priority has been building financial stability frameworks that improve macroeconomic monitoring, financial cooperation, and cross-border policy coordination among member states.

At the regional level, stronger regional coordination has also supported deeper economic integration, particularly through mechanisms under the ASEAN Economic Community. In parallel, ASEAN has improved its crisis response capability through initiatives such as the Chiang Mai Initiative, which helps provide liquidity support during financial stress.

| Explore how to invest in ASEAN in 2026 with our detailed guide! |

Misread #4: Ignoring The Structural Rise of Asean’s Digital Economy

ASEAN’s economic outlook is increasingly shaped by structural changes in the digital economy. Across the region, digital services, platforms, and infrastructure are becoming important drivers of growth alongside traditional sectors.

Digital economy as growth stabilizer

ASEAN’s digital economy is becoming a key growth pillar, expanding alongside manufacturing and trade as internet access improves across Southeast Asia. According to the Google e-Conomy SEA report, the region’s digital economy reached about USD 218 billion in 2023 and could approach USD 600 billion by 2030. Growth is driven by three developments:

- E-commerce platforms: Rising online retail adoption across Indonesia, Vietnam, Thailand, and the Philippines.

- Fintech adoption: Digital wallets and mobile payments expanding financial access.

- Cross-border digital services: Cloud platforms and digital logistics enabling regional business operations.

Tech investment and data infrastructure

Investment in digital infrastructure across ASEAN has accelerated as both governments and private investors expand the foundations of a digital economy. Several developments are particularly notable:

- Data center expansion: Large facilities are being built in Singapore, Malaysia, Indonesia, and Thailand to support growing demand for cloud computing and AI services.

- Digital payment ecosystems: Mobile wallets and real-time payment systems now serve hundreds of millions of users across Southeast Asia.

- Startup ecosystem growth: Fintech, logistics technology, and enterprise software startups are expanding rapidly.

Together, these investments strengthen regional digital capacity and support more efficient cross-border business operations.

Digitalization and economic resilience

Digital transformation is strengthening economic resilience strategies across ASEAN as digital services and technology firms continue to expand. As a result, many economies are developing a diversified revenue base, supported by e-commerce, digital services, and platform-based business models.

At the same time, the rise in digital sectors reduces reliance on export manufacturing. Companies can more easily access local markets through online tools and digital systems, creating more steady and stable economic growth across the region.

| To better understand how infrastructure and industrial development support ASEAN’s long-term resilience, explore our analysis of ASEAN’s infrastructure development and investment opportunities. |

ASEAN’s digital economy is expanding rapidly across e-commerce, fintech, and digital services.

This shift is visible in several areas:

- Stronger banking regulation: Capital requirements and supervisory standards have improved across many financial systems.

- Flexible currency management: Exchange rates are allowed to adjust to global shocks instead of creating sudden financial stress.

- Macroprudential frameworks: Authorities monitor credit growth, capital flows, and financial risks more closely.

Crisis track record

ASEAN’s current policy capacity has been shaped by past economic shocks. After the Asian Financial Crisis (1997–1998), many governments strengthened financial supervision, improved banking regulation, and increased foreign-exchange reserves to stabilize their financial systems.

More recently, the COVID-19 pandemic and commodity shocks tested these frameworks again. Governments introduced fiscal stimulus, monetary support, and targeted business assistance. According to the ASEAN Secretariat, regional initiatives under the ASEAN Comprehensive Recovery Framework supported economic recovery, showing that short-term volatility does not necessarily signal structural fragility.

What Recognizing ASEAN’s Economic Resilience Means for US Executives

Recognizing ASEAN’s economic resilience strategies reshapes corporate strategy, positioning the region as a structural partner for diversification, investment, and risk management rather than a temporary alternative.

Strategic implications for US economic resilience planning

Recognizing ASEAN’s economic resilience has direct implications for corporate strategy. For many U.S. companies, the region is becoming a practical component of supply chain diversification, rather than a secondary production location.

In strategic terms, ASEAN offers several advantages:

- More diversified supply chains, reducing exposure to concentration risks in a single market

- New investment opportunities across manufacturing, digital services, and regional logistics

- More realistic risk modeling, reflecting ASEAN’s institutional and economic stability

As global supply networks adjust, ASEAN can contribute directly to U.S. economic resilience strategies through geographic diversification.

Rethinking emerging markets strategy

For many multinational firms, ASEAN has traditionally been viewed as a tactical hedge when supply chain disruptions occur. However, this perception is gradually changing.

Today, the region increasingly operates as a structural partner in global production networks. Integrated manufacturing clusters, growing consumer markets, and stronger digital infrastructure support this role. Thus, companies that recognize this shift can build more stable regional strategies, combining manufacturing, sourcing, and market access across ASEAN rather than using the region only as a temporary alternative.

Where misreading ASEAN creates competitive disadvantage

Misinterpreting ASEAN’s economic trajectory can create strategic blind spots. Companies that underestimate the region may overlook emerging opportunities or misjudge operational risks. Common consequences include:

- Missed first-mover advantage in fast-growing sectors and new industrial zones across the region.

- Overexposure to single markets, which increases vulnerability to geopolitical or trade disruptions.

- Incorrect risk assumptions, often caused by viewing ASEAN as a uniform market rather than a diverse regional system.

A more accurate understanding of ASEAN’s economic resilience strategies helps companies build more balanced global strategies and reduce unnecessary concentration risks.

Conclusion

ASEAN’s economic resilience is increasingly structural rather than opportunistic. It is supported by several long-term factors, including diversified economies, expanding regional integration, responsive policy frameworks, strong domestic demand, and ongoing digital transformation across ASEAN.

For international companies, these conditions create a more stable environment for manufacturing, sourcing, and market expansion. U.S. executives can gain clearer strategic insight when evaluating supply chain diversification and long-term investment opportunities in ASEAN.

At Source of Asia, we support companies evaluating and entering ASEAN markets through market research, partner identification, and operational advisory. Our team helps businesses navigate regional complexity while building practical, long-term strategies in Southeast Asia.

| Are you planning to expand or invest in ASEAN? Contact our team to discuss your strategy and receive tailored insights for your target markets. |

Frequently Asked Questions

Economic resilience refers to an economy’s ability to withstand shocks and maintain stable growth during disruptions such as financial crises, geopolitical tensions, or supply chain interruptions. In emerging markets, it typically relies on diversified industries, sound financial regulation, flexible policy responses, and stable domestic demand.

ASEAN economies benefit from diversified trade partnerships, regional supply chain integration, and growing domestic markets. These structural factors help the region adapt to global economic shifts while maintaining relatively stable growth.

ASEAN provides multiple production and sourcing locations across different countries, allowing companies to diversify manufacturing and reduce supply chain concentration risks.

ASEAN is better viewed as a diverse growth region. Some economies remain emerging, while others, such as Singapore, Malaysia, Thailand, and Vietnam already host established manufacturing sectors and integrated supply chains.