The China Plus One (China + 1) strategy has become a practical response to supply chain concentration risk. Rising labor costs, demographic shifts, geopolitical tensions, and pandemic disruptions have pushed companies to diversify part of their manufacturing footprint beyond China. The objective is risk balance. Southeast Asia has therefore gained strategic importance in global production planning.

Within ASEAN, Vietnam stands out under the China Plus One strategy thanks to competitive labor costs, geographic proximity to China, a strong FTA network, and expanding industrial infrastructure. For manufacturers seeking resilience without sacrificing market access, Vietnam represents a structured diversification option.

Key Insights

-

The China Plus One strategy reduces concentration risk rather than replacing China.

-

Geopolitical and structural cost factors continue to accelerate supply chain diversification.

-

Vietnam combines cost competitiveness, logistics proximity, and broad trade agreement coverage.

-

More than 15 major FTAs enhance Vietnam’s export access and supply chain integration.

-

Regional economic zones in Vietnam offer differentiated advantages depending on strategy.

-

Effective implementation requires evaluating infrastructure, labor stability, incentives, and scalability.

What is the China+1 Strategy?

The China Plus One strategy, often referred to as C+1, is a supply chain diversification approach. Instead of relying solely on China, companies expand production or sourcing into additional Asian markets, particularly in Southeast Asia. As global supply chains face geopolitical pressure and cost adjustments, diversification has shifted from optional to strategic. Businesses are now actively reducing single-country dependency while maintaining operational flexibility.

Why the China Plus One Strategy Has Gained Momentum

Several structural shifts have reinforced this diversification trend.

Social & demographic changes in China

During the early phase of China’s industrialization, low labor costs supported rapid manufacturing expansion. However, over time, wages increased as living standards improved and industries matured.

At the same time, demographic pressures intensified. The legacy of the one-child policy led to an aging population and a shrinking workforce. According to China’s National Bureau of Statistics, in 2013, the population decreased by 2.4 million. As labor supply tightened, production costs rose. Consequently, manufacturers began exploring alternative production bases in Southeast Asia, where labor costs remained competitive.

U.S.–China trade war and EU–China tension

Geopolitical tensions have accelerated diversification decisions.

In 2018, the United States imposed tariffs on hundreds of billions of dollars of Chinese goods. China responded with retaliatory measures. As a result, companies exporting to the U.S. faced rising costs. Vietnam quickly emerged as a major beneficiary. U.S. imports from Vietnam increased from USD 49.1 billion in 2018 to USD 66.5 billion in 2019, representing strong year-on-year growth.

U.S.–China trade war and EU–China tension

Meanwhile, tensions between China and the European Union, including sanctions related to Xinjiang, further increased regulatory uncertainty. Visa cancellations and residence bans were promulgated. The United Kingdom and the United States followed suit. China immediately fought back by applying similar sanctions. This environment encouraged firms to reassess supply chain concentration risks.

Covid-19 and supply chain disruption

The Covid-19 pandemic exposed the vulnerability of centralized manufacturing models. Lockdowns, port closures, and transport restrictions disrupted global production flows. Moreover, China’s Zero-COVID policy intensified supply chain uncertainty. As a result, companies reconsidered heavy reliance on a single production base.

Since then, supply chain diversification into Southeast Asia has accelerated across multiple industries, including:

-

Indonesia for information and communication technology

-

Malaysia for electrical and electronics

-

Thailand for automotive and electronics

-

Vietnam for low- and mid-tech manufacturing

Why Vietnam Stands Out in the China Plus One Strategy

Among Southeast Asian markets, Vietnam has emerged as one of the most strategic alternatives. However, while Vietnam offers clear advantages, investors must also assess structural constraints.

| Conveniences of Vietnam | Improvement items |

|

|

| Upcoming upgrade in its China+1 position | Caution Zones |

|

|

Competitive labor market

Vietnam remains one of the most competitive labor markets in Southeast Asia. Vietnam has 4 different wages, which are divided into 4 regions. The following compares wages in Vietnam with those in neighbouring countries. Let’s take a look!

| Region 1 | Region 2 | Region 3 | Region 4 |

| Includes the urban and suburban areas: Hanoi, Hai Phong, Ho Chi Minh City, and the provinces of Dong Nai, Binh Duong, and Ba Ria – Vung Tau. | Rural areas: Hanoi, Ho Chi Minh City, and medium-sized cities like Da Nang, Nha Trang, and Can Tho. | Smaller cities and suburban districts. | All remaining areas.

|

| Minimum monthly wage: USD 189 | Minimum monthly wage: USD 168 | Minimum monthly wage: USD 147 | Minimum monthly wage: USD 131 |

Compared with neighboring countries:

- Malaysia: USD 270–295

- Thailand: USD 248–265

- Indonesia: USD 120–298

- Cambodia: USD 190 minimum

Although wage inflation is gradually increasing, Vietnam continues to offer cost efficiency relative to developed manufacturing hubs.

Geographic proximity to China

Vietnam’s location offers logistical advantages.

For example, Hai Phong is approximately 537 miles from Shenzhen, one of China’s major manufacturing hubs. In contrast, Bangkok, Phnom Penh, Kuala Lumpur, and Jakarta are significantly farther. (Bangkok in Thailand (1,708 miles), Phnom Penh in Cambodia (1,716 miles), Kuala Lumpur in Malaysia (1,879 miles), or Jakarta in Indonesia (2,050 miles).

Because of this proximity, companies can maintain supplier relationships in China while shifting part of their production to Vietnam. This model reduces disruption while improving diversification.

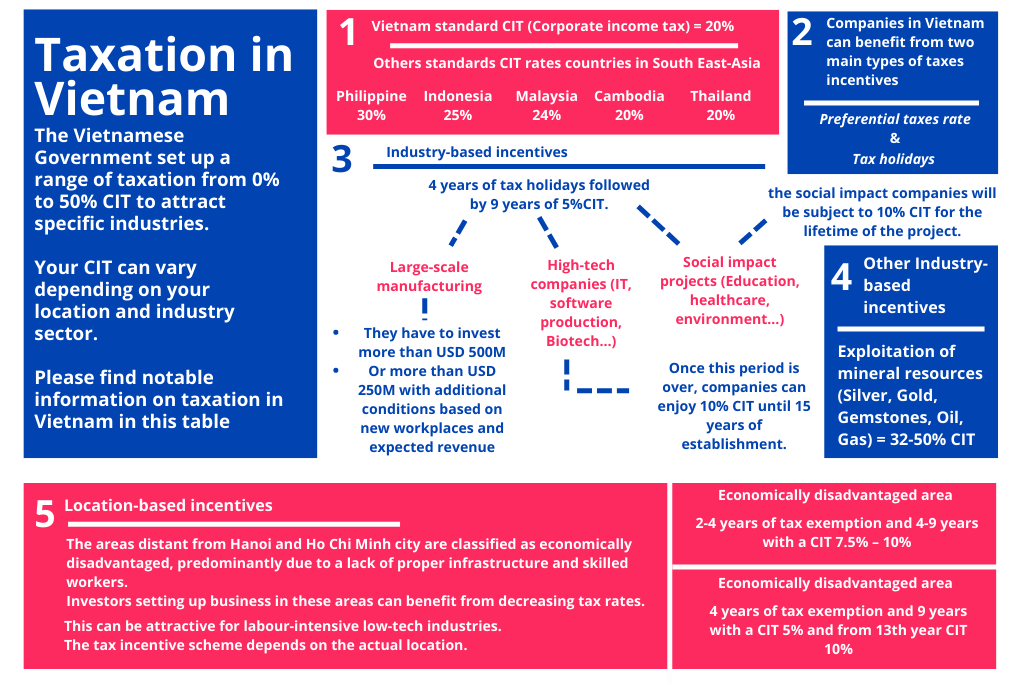

Preferential taxation and economic zones

Vietnam provides incentive schemes through:

-

Corporate income tax reductions

-

Economic Zones

Taxation in Vietnam. Source: Cekindo

Three major Key Economic Zones support foreign direct investment:

- North Key Economic Zone (NKEZ)

- Central Key Economic Zone (CKEZ)

- South Key Economic Zone (SKEZ)

Each zone presents distinct advantages and trade-offs in infrastructure, supplier density, and logistics capacity. Therefore, site selection must align with industry strategy rather than cost alone. Below is a table summarizing Vietnam’s Economic Zones.

| (Sources: Vietnam Briefing) | NKEZ | CKEZ | SKEZ |

| Key provinces | Bac Ninh, Hai Duong, Hai Phong, and Hanoi | Quang Ngai, Hue, Da Nang | Long An, Binh Duong, Dong Nai, and Ho Chi Minh City |

| Pros | Proximity to China reduces logistics costs for imports from China | Low costs, encourages clean energy to settle, and large land availability | Diversified supply base and proximity to the rest of Southeast Asia |

| Cons | A less diversified labor force and industries than the SKEZ | Still a lack of infrastructure and technology industry players | Congested logistic networks |

| Investment strategy | Companies seeking to quickly relocate operations and seeking a high level of integration with Chinese supply chains | Companies seeking low costs, a long-term investment strategy, and are willing to relocate the majority of their supply chain over time | Companies seeking to diversify their supply chain and distribution network, and companies interested in targeting the domestic market |

Risks and caution zones

Despite its advantages, Vietnam faces structural challenges:

-

Infrastructure capacity gaps

-

Supplier density is lower than in China

-

Rising wages in major industrial provinces

-

Logistics congestion in southern hubs

As a result, Vietnam should be viewed as part of a diversified strategy rather than a complete replacement for China.

Vietnam’s FTA Network: A Structural Driver in the China Plus One Strategy

Vietnam’s Free Trade Agreement network is one of its strongest structural advantages in a China Plus One strategy.

The country has signed and implemented more than 15 major FTAs, covering over 50 economies. These include ASEAN Free Trade Area, CPTPP, EVFTA, UKVFTA, RCEP, and bilateral agreements with South Korea, Japan, and other strategic partners.

This network provides preferential tariff access to markets representing a significant share of global GDP and trade flows. For manufacturers relocating production to Vietnam, this means broader export access under reduced tariff regimes compared to many competing locations.

Vietnam’s import and export turnover, balance of trade in the period from 2012 to 2019

FDI performance reflects this integration. Over the past two decades, annual foreign direct investment inflows increased multiple times compared to the mid-2000s. In several years, the foreign-invested sector accounted for around 20% of GDP and more than half of total export turnover.

Beyond tariff reductions, FTAs have contributed to regulatory upgrades, stronger investment protection, and improved customs procedures. These structural improvements reduce friction in cross-border trade and enhance supply chain reliability.

Within a China Plus One (China + 1) framework, Vietnam’s trade architecture allows companies to diversify production while maintaining preferential access to major export markets. This strengthens Vietnam’s position as a strategic manufacturing node in Southeast Asia rather than merely a low-cost alternative.

Vietnam FTAs Network (Source: Asia Business Consulting). APEC: Asia-Pacific Economic Cooperation; VEGETA: Vietnam Eurasian Union FTA; EU: European Union; CPTTP: Comprehensive and Progressive Agreement for Trans-Pacific Partnership; ASEAN: Association of Southeast Asian Nations; RCEP: Regional Comprehensive Economic Partnership

Final Thoughts

The China Plus One strategy does not eliminate China from global supply chains. China remains a major manufacturing center with advanced infrastructure and industrial depth. Instead, the strategy focuses on reducing concentration risk while preserving operational efficiency.

In this context, Southeast Asia has gained strategic relevance. Among ASEAN markets, Vietnam combines competitive labor costs, geographic proximity to China, a broad FTA network, and expanding industrial capacity. For companies seeking to reinforce supply chain resilience, Vietnam can serve as a practical pillar within a broader diversification strategy.

If you are assessing how to structure your China Plus One (China + 1) roadmap in Southeast Asia, our experts at Source of Asia can help you evaluate market entry options, site selection, regulatory considerations, and supply chain alignment.

👉 Contact us at hello@sourceofasia.com to discuss your diversification strategy.