Introduction

In 2026, the ASEAN bloc continues to attract global expansion strategies due to its manufacturing growth, rising consumer demand, and increasing role in global supply chains. Many businesses view ASEAN-6 as a connected regional opportunity that can support diversification, production scaling, and long-term market growth.

However, companies often underestimate how differently ASEAN markets operate in practice. Regulatory frameworks, labor dynamics, infrastructure quality, and execution timelines vary significantly between countries such as Singapore, Vietnam, and Indonesia. Applying the same operating model across multiple markets frequently leads to compliance delays, unexpected costs, and slower expansion execution.

In this article, we, Source of Asia, explain why ASEAN-6 markets operate differently, what businesses commonly misunderstand about the ASEAN bloc, and how companies can approach regional expansion more effectively.

Key Insights

- ASEAN offers growing regional integration, but business execution remains highly fragmented across countries.

- Economic indicators do not reflect real execution differences in labor, infrastructure, and regulation.

- Scaling across ASEAN-6 requires market-specific adaptation due to structural and behavioral differences.

- Regulatory and operational conditions vary significantly despite regional cooperation frameworks.

- Successful expansion depends on country-level execution rather than a unified regional model.

What Is the ASEAN Bloc and Why Does It Matter for Businesses?

The ASEAN bloc creates major regional opportunities for trade, manufacturing, and expansion. However, businesses must also understand how ASEAN integration works differently in practice across each market.

What defines the ASEAN bloc

The Association of Southeast Asian Nations is a regional cooperation framework established to strengthen trade integration, investment flows, and economic cooperation across Southeast Asia. Today, the ASEAN bloc includes 11 member economies: Singapore, Vietnam, Cambodia, Indonesia, Laos, Malaysia, Myanmar, the Philippines, Thailand, Brunei, and Timor-Leste. The framework mainly supports:

- Trade facilitation between member markets

- Cross-border investment and regional supply chains

- Tariff reduction and economic cooperation

However, ASEAN is not a unified operating market. Each country still maintains different legal systems, tax policies, labor regulations, licensing procedures, and foreign ownership rules. As a result, businesses often need separate market entry and execution strategies across ASEAN markets.

The ASEAN bloc supports regional trade, investment, and cross-border economic cooperation.

Why ASEAN attracts global expansion strategies

The ASEAN bloc continues to attract global investors because of its strong long-term growth potential and strategic role in global supply chains. Despite weaker global investment conditions, ASEAN recorded a record US$230 billion in FDI inflows in 2023, reflecting continued investor confidence across the region. Looking ahead, according to McKinsey Company, annual FDI inflows are projected to exceed US$300 billion between 2024 and 2030.

Several factors continue driving expansion into ASEAN markets:

- Growing middle-class consumer demand

- Expanding manufacturing and export capacity

- Strategic supply chain diversification across Asia

- Rapid digital and industrial development

Thus, businesses increasingly evaluate ASEAN based on operational resilience, industrial capability, and long-term scalability, rather than low-cost manufacturing alone.

| Understanding ASEAN investment dynamics requires a closer look at entry timing and market readiness. 👉 Explore key insights on investing in ASEAN. |

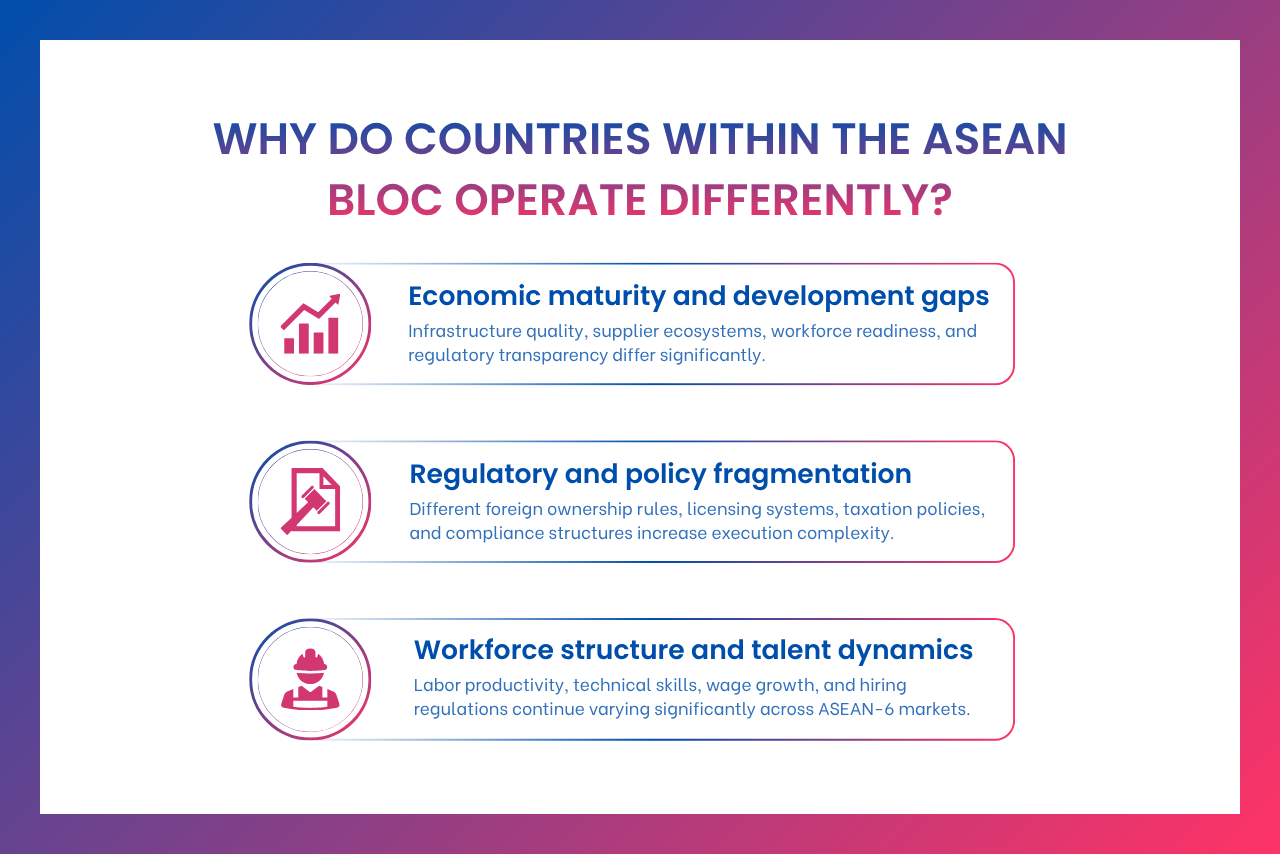

Why Do Countries Within The ASEAN Bloc Operate Differently?

Although ASEAN markets are regionally connected, operational conditions still vary significantly between countries. Economic maturity, regulatory structures, and workforce dynamics continue shaping how businesses execute and scale across ASEAN-6.

Economic maturity and development gaps

One of the biggest differences across ASEAN-6 comes from uneven economic development and industrial maturity. Although the region is often grouped, each market operates at a different stage of economic growth and business capability. For example:

| Market | Typical Economic Profile |

| Singapore | Advanced service and financial economy |

| Vietnam | Rapid industrial and manufacturing growth |

| Indonesia | Large domestic consumption economy |

| Thailand | Mature industrial manufacturing base |

| Malaysia | Mixed industrial and service specialization |

| Philippines | Service and BPO-driven economy |

Hence, execution conditions across ASEAN-6 remain highly uneven. Infrastructure quality, logistics capability, supplier ecosystems, workforce readiness, and regulatory transparency differ significantly between markets. Therefore, businesses expanding across the ASEAN bloc often need country-specific operating and execution strategies rather than applying one standardized regional model.

Regulatory and policy fragmentation

Regulatory fragmentation remains a major operational challenge across the ASEAN bloc. Although regional integration has improved trade cooperation, each ASEAN market still applies different rules for foreign ownership, licensing, taxation, and compliance.

For example, Indonesia allows up to 100% foreign ownership in certain banking structures, while Vietnam and Thailand generally cap foreign bank ownership at 49%, creating different market entry conditions for investors.

As a result, execution complexity increases significantly across ASEAN-6. Businesses operating in multiple markets often face longer approval timelines, heavier compliance burdens, and unexpected administrative costs due to varying regulatory structures and local enforcement practices.

Workforce structure and talent dynamics

Workforce conditions vary significantly across ASEAN-6, particularly in labor productivity, technical skills, wage growth, language capability, and hiring regulations. For instance, Singapore offers a highly skilled workforce in finance, technology, and regional management, while Indonesia provides a large labor pool but may require more localized workforce management across different regions and provinces.

Simultaneously, lower labor costs may be offset by higher turnover, training requirements, or administrative inefficiencies. Localization policies also affect hiring strategies in several ASEAN markets. Thus, talent quality and workforce stability increasingly influence long-term operational competitiveness across the region.

ASEAN countries operate differently due to economic, regulatory, and workforce structure differences.

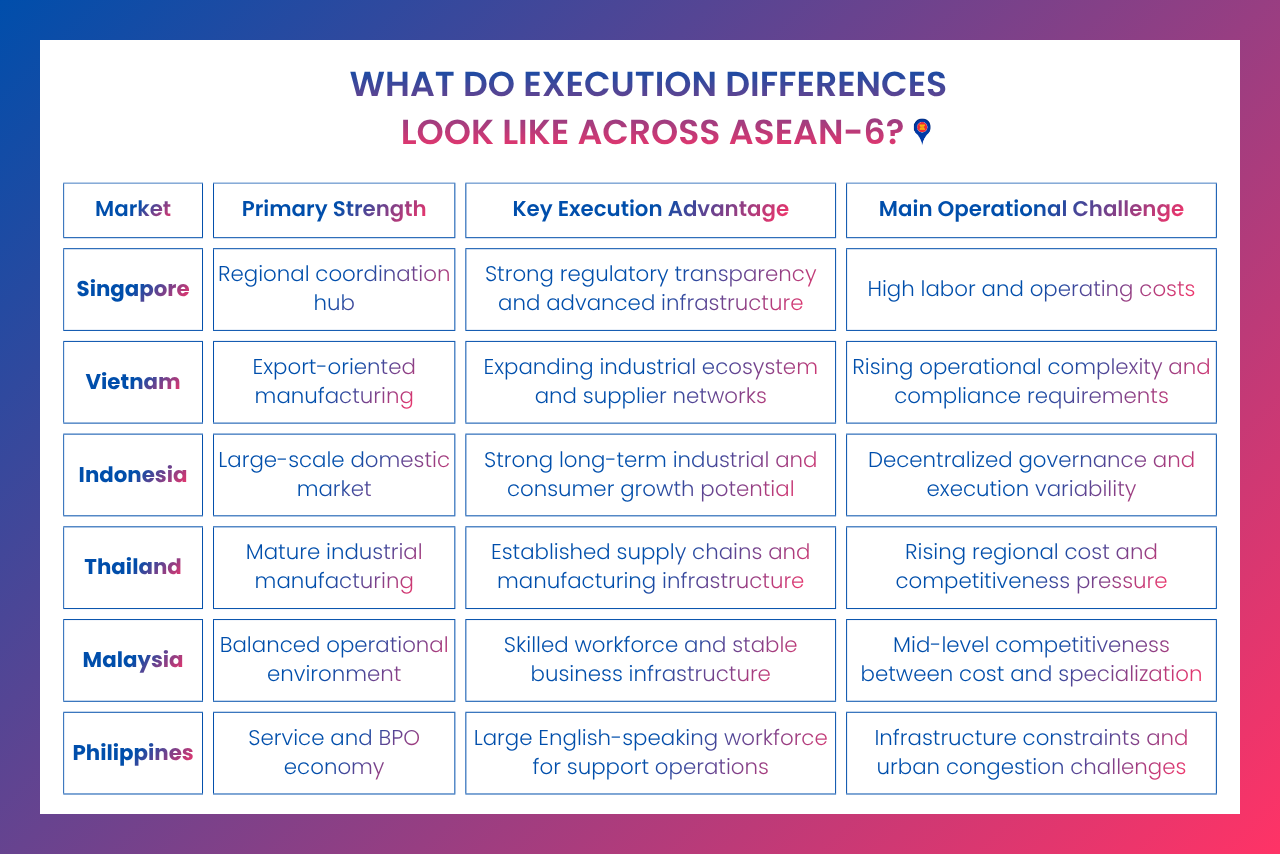

What Do Execution Differences Look Like Across ASEAN-6?

Although ASEAN-6 markets are regionally connected, execution conditions vary significantly in cost structure, infrastructure, regulatory coordination, and operational scalability across each country.

Singapore: Control and regional coordination

Singapore remains one of the main regional coordination and headquarters hubs within the ASEAN bloc. Many multinational companies use Singapore to manage:

- Regional leadership and governance

- Financial and treasury operations

- Investment structuring

- Cross-border supply chain coordination

The market offers several operational advantages, including high regulatory transparency, strong legal protection, advanced infrastructure, and efficient administrative systems. Hence, Singapore is often used for regional control and strategic management functions.

However, the country also operates with a premium cost structure. Labor expenses, office rental, and operational overhead remain significantly higher than in many other ASEAN markets, making Singapore less suitable for cost-sensitive operations.

Vietnam: Manufacturing growth with rising complexity

Vietnam has become one of SEAN’s most dynamic manufacturing markets. The country is supported by strong export positioning and an expanding industrial ecosystem. Key advantages include:

- Competitive labor structure

- Expanding industrial zones

- Strong export-oriented manufacturing

- Growing supplier and production networks

In addition, the market is becoming more operationally complex as industrial activity continues to expand. Businesses increasingly face rising wages, stronger labor competition, and evolving compliance requirements across industries. Therefore, while Vietnam remains highly attractive for industrial expansion, companies often require strong local execution capabilities and operational coordination to scale efficiently.

Indonesia: Scale with execution variability

Indonesia remains one of the most important growth markets in the ASEAN bloc because of its large domestic economy and long-term industrial potential. The country continues attracting investment across manufacturing, consumer sectors, natural resources, and digital industries due to its expanding middle-class population and market scale.

At the operational level, execution conditions are often less standardized than in smaller ASEAN markets. Regional administrative differences, decentralized governance, infrastructure gaps, and licensing variability can create uneven business environments across provinces. Consequently, companies entering Indonesia often require strong local coordination and market-specific execution planning to manage operational complexity effectively.

Thailand: Established industrial ecosystem under pressure

Thailand has long been one of ASEAN’s strongest industrial manufacturing hubs, particularly in automotive production, electronics, and export-oriented industries. The country benefits from mature infrastructure, experienced suppliers, and well-developed industrial ecosystems that support large-scale manufacturing operations. Key industrial strengths include:

- Automotive manufacturing

- Electronics production

- Industrial supply chains

- Export-oriented manufacturing

Simultaneously, neighboring ASEAN markets continue improving manufacturing capacity and cost competitiveness. Consequently, businesses increasingly evaluate productivity, supply chain stability, and operational efficiency alongside labor cost positioning when assessing Thailand’s long-term manufacturing advantages.

Malaysia: Balanced capability and specialization

Malaysia offers a balanced operating environment within ASEAN-6 through its mid-cost structure, skilled workforce, and relatively stable business infrastructure. The market is often considered suitable for companies seeking operational efficiency without the higher cost structure of more developed regional hubs.

Malaysia also maintains strong sector specialization in several industries, particularly:

- Electronics manufacturing

- Shared and business services

- Technology-related operations

- Professional support services

In addition, the country generally provides a more stable regulatory environment than some neighboring ASEAN markets, helping businesses maintain greater operational predictability during regional expansion.

Philippines: Service-driven and talent-led

The Philippines continues expanding its position as a service-driven economy, particularly in BPO operations, customer support services, and digital business functions. Its large English-speaking workforce gives the country a strong advantage for international companies managing regional support and back-office operations across ASEAN.

Concurrently, operating conditions can vary depending on infrastructure quality and urban density. Businesses may encounter logistics constraints, administrative inefficiencies, and congestion challenges in major cities. Under these conditions, careful location planning and infrastructure assessment often become important parts of long-term operational setup.

| Execution differences across ASEAN-6 become more visible when examined through country-level operating conditions and real market structures. 👉 View detailed ASEAN country profiles for market-specific data. |

Execution conditions across ASEAN-6 vary in infrastructure, scalability, logistics, and operational coordination.

Why Cost Advantages Differ Across ASEAN-6 Markets

Many businesses still evaluate the ASEAN bloc primarily through labor cost comparisons. Yet in practice, overall operating efficiency across ASEAN-6 is influenced by infrastructure quality, regulatory conditions, logistics capability, and execution complexity. Several factors commonly shape these cost differences:

- Labor cost differences are only part of the equation: Workforce productivity, infrastructure quality, supplier maturity, and logistics efficiency often influence operating performance as much as wage levels themselves. For instance, Singapore operates with higher labor costs but offers stronger infrastructure, administrative efficiency, and business predictability than many lower-cost ASEAN markets.

- Operational inefficiencies can offset labor savings: Lower labor costs may eventually be outweighed by delays, training requirements, compliance workload, inventory inefficiencies, or management complexity during execution. In some ASEAN markets, administrative delays or fragmented supplier ecosystems can gradually increase total operational expenses over time.

- Multi-country coordination increases hidden costs: Businesses operating across ASEAN-6 often manage different legal systems, localization policies, supplier structures, and reporting requirements simultaneously. This creates additional coordination pressure across regional operations, particularly when execution standards and regulatory practices differ significantly between markets.

| Cost competitiveness in ASEAN is shifting beyond wage levels and requires a structural view of operations. 👉 Read how ASEAN is evolving beyond low-cost positioning. |

What Businesses Often Get Wrong About ASEAN Expansion

Market perceptions of the ASEAN bloc often overlook how differently countries operate in practice despite regional economic linkages. These gaps between perception and execution frequently lead to incorrect assumptions in expansion planning, operational design, and market entry strategy. There are four recurring misunderstandings:

- ASEAN operates as a single unified market

Economic integration across ASEAN supports stronger trade flows, investment mobility, and cross-border collaboration. However, each country continues to operate under distinct legal systems, tax frameworks, licensing procedures, and administrative processes. This creates structural differences in how businesses are established and managed, requiring localized compliance and operational planning in each market. - Similar growth rates mean similar execution conditions

Macroeconomic indicators across ASEAN-6 can appear aligned, but execution realities differ significantly on the ground. Labor availability, infrastructure readiness, regulatory enforcement, and supplier ecosystem maturity vary widely between markets. These differences directly affect project timelines, operational stability, and scalability potential. - Regional expansion scales evenly across ASEAN-6

A business model proven in one ASEAN market cannot be directly replicated in another without adjustment. Differences in logistics networks, consumer behavior, distribution structures, and operational maturity mean that scaling requires market-specific adaptation rather than replication. - Regulatory integration is fully harmonized in practice

Although regional agreements aim to improve harmonization, foreign ownership restrictions, approval timelines, and compliance requirements still differ significantly across countries. These variations directly impact market entry speed, cost structure, and overall execution complexity.

| Investor interpretation of ASEAN resilience varies depending on market entry strategy and sector exposure. 👉 Discover how US executives reassess ASEAN economic resilience. |

Why ASEAN-6 Markets Cannot Be Managed as One Operating Model

Regional expansion in the ASEAN bloc requires adaptation at the country level rather than a unified operating approach. While the region is economically connected, execution conditions differ significantly across markets in practice. Four key reasons explain this:

- Different markets require different execution timelines: Setup speed, licensing processes, and regulatory approvals vary by country, which directly impacts how fast businesses can enter and scale operations.

- Regulatory alignment does not mean operational alignment: Even with regional agreements, each country maintains distinct enforcement standards, compliance requirements, and administrative procedures.

- Local channel structures shape market behavior differently: Distribution networks, partner ecosystems, and sales channels are highly localized, influencing how products and services actually reach the market.

- Regional strategy must adapt country by country: Differences in infrastructure, labor conditions, and business ecosystems require tailored execution models rather than a single standardized approach.

Conclusion

In conclusion, ASEAN-6 offers strong regional potential, but it does not operate as a uniform business environment. Each market follows different regulatory systems, levels of economic development, and operational structures, which directly affect how companies plan entry, manage execution, and scale operations. For businesses, this means regional expansion must be approached with a country-specific perspective rather than a single ASEAN-wide model.

At Source of Asia, we support companies in navigating these differences through practical market entry advisory, regulatory and operational assessments, and on-the-ground execution support across Southeast Asia. Our focus is on helping businesses reduce uncertainty, align strategy with local conditions, and build sustainable operations in each target market.

| 👉Connect with us to turn ASEAN complexity into a clear, executable market entry strategy. |

Frequently Asked Questions

ASEAN is a regional organization of Southeast Asian countries focused on economic cooperation, trade facilitation, and investment flows. Although integrated at the economic level, each member country maintains independent legal, tax, and regulatory systems, which affect business operations.

The ASEAN bloc provides access to a large, fast-growing market, but scaling requires adaptation. Differences in regulation, infrastructure, and execution conditions mean companies must adjust strategies by country instead of applying a single regional model.

There is no universal best market. Singapore is often used for regional HQ functions, Vietnam for manufacturing, Indonesia for scale, and Malaysia or Thailand for balanced industrial operations. Selection depends on business objectives and operating model.

A key mistake is treating ASEAN as a unified market. Companies often underestimate regulatory fragmentation, execution complexity, and local market differences, leading to misaligned strategies and inefficient regional expansion planning.